Finance and Accounting Articles – Blog Categories

Quick Summary

- Understand the foundational definition of financial acumen.

- Learn the core components and their significance in business.

- Discover practical steps to enhance your financial intelligence.

What is Financial Acumen? The Foundational Definition

Financial acumen refers to the ability to understand and apply financial principles in a way that enhances decision-making and drives business success. It encompasses a range of skills, including the ability to interpret financial statements, analyze financial data, and make informed decisions based on that analysis. Financial acumen is not just about numbers; it involves understanding the broader economic context in which a business operates and how financial decisions impact overall performance.

Core Components of Financial Acumen

To develop financial acumen, one must understand several core components:

* Financial Statements: Understanding balance sheets, income statements, and cash flow statements is fundamental. These documents provide insights into a company’s financial health and operational efficiency.

* Budgeting and Forecasting: The ability to create budgets and forecast future financial performance is essential for strategic planning and resource allocation.

* Cost Management: Knowing how to manage costs effectively can lead to improved profitability and operational efficiency.

* Investment Analysis: Evaluating potential investments and understanding their risks and returns is crucial for making sound financial decisions.

* Market Understanding: A grasp of market dynamics, including competition and economic trends, helps in making informed strategic choices.

Why is Financial Acumen Essential for Non-Finance Roles?

Financial acumen is not just for finance professionals; it is increasingly important for individuals in non-finance roles. Here’s why:

* Enhanced Decision-Making: Employees with financial acumen can make better decisions that align with the company’s financial goals.

* Cross-Functional Collaboration: Understanding financial implications fosters better communication and collaboration across departments.

* Career Advancement: Professionals who demonstrate financial acumen are often seen as more valuable and are more likely to be considered for leadership roles.

The Importance of Financial Acumen in the Workplace

In the workplace, financial acumen plays a vital role in:

* Strategic Planning: It aids in developing strategies that are financially viable and sustainable.

* Performance Measurement: Financial acumen allows for the assessment of business performance against financial goals.

* Risk Management: Understanding financial risks helps organizations mitigate potential losses and capitalize on opportunities.

The Core Distinction: Financial Acumen vs. Financial Literacy

While financial acumen and financial literacy are often used interchangeably, they are distinct concepts:

* Financial Acumen: Involves a deeper understanding of financial principles and their application in business decision-making.

* Financial Literacy: Refers to the basic understanding of financial concepts, such as budgeting and saving, which is essential for personal finance management.

How to Develop and Improve Financial Acumen

Improving your financial acumen requires a proactive approach:

* Education: Take courses in finance, accounting, or business management to build foundational knowledge.

* Practical Experience: Seek opportunities to work on financial projects or collaborate with finance teams.

* Mentorship: Find a mentor with strong financial expertise who can provide guidance and insights.

* Continuous Learning: Stay updated on financial trends and best practices through reading, webinars, and workshops.

Practical Steps to Build Financial Intelligence

To build your financial intelligence, consider the following practical steps:

1. Read Financial News: Stay informed about market trends and economic developments.

2. Analyze Financial Reports: Regularly review your organization’s financial statements to understand performance metrics.

3. Engage in Financial Discussions: Participate in discussions about financial strategies and outcomes with colleagues.

4. Utilize Financial Tools: Familiarize yourself with financial software and tools that can aid in analysis and reporting.

When is Financial Acumen Most Critical?

Financial acumen becomes particularly critical during:

* Budgeting Cycles: When planning for the upcoming fiscal year, understanding financial implications is essential.

* Mergers and Acquisitions: Evaluating potential deals requires strong financial analysis skills.

* Crisis Management: In times of financial distress, having a solid grasp of financial principles can guide recovery efforts.

| Feature | Financial Acumen | Financial Literacy |

|---|---|---|

| Definition | Ability to understand and apply financial principles | Basic understanding of financial terms and concepts |

| Application | Strategic decision-making and business insights | Personal finance management |

| Target Audience | Professionals in various roles | Individuals seeking basic financial knowledge |

Comparison of key aspects.

Critical Business Moments Requiring Strong Financial Acumen

Certain business moments demand heightened financial acumen:

* Launching New Products: Understanding the financial implications of product development and marketing is crucial.

* Entering New Markets: Financial analysis helps assess the viability and risks of expansion.

* Cost-Cutting Initiatives: Making informed decisions about where to cut costs without sacrificing quality requires financial insight.

Frequently Asked Questions (FAQ)

Q: Is financial acumen only for managers and executives?

Q: How can I measure my team’s financial acumen?

Q: Does financial acumen mean I need to become an accountant?

Q: What resources are available to improve financial acumen?

Q: How does financial acumen impact team collaboration?

Q: Can financial acumen be developed over time?

## Unlock Your Potential with LBTA

At LBTA, we understand the importance of financial acumen in today’s business landscape. Our comprehensive training programs are designed to equip professionals with the skills and knowledge necessary to excel in their roles. Whether you’re looking to enhance your financial understanding or develop your team’s capabilities, our expert-led courses provide the insights you need to succeed. Join us today and take the first step towards mastering financial acumen!

What Is Long-Term Financial Planning?

Before diving into the steps in long-term financial planning, it’s important to understand what the concept really means. Long-term financial planning is the process of setting and working toward financial goals that span years—or even decades. It’s about building a solid foundation for your future, not just managing your money today. Here’s what it typically involves:

Defining future financial goals: These could include retirement, children’s education, buying a home, or starting a business.

Projecting income and expenses: Estimating future earnings and costs to see what’s realistic and where adjustments are needed.

Creating a personalized investment strategy: Choosing savings and investment vehicles that match your risk tolerance and timeline.

Factoring in inflation and life changes: Planning for the unknown by considering rising costs and shifting priorities.

Reviewing and adjusting regularly: Like any plan, it needs to evolve with your life and financial situation.

Understanding this foundation makes it easier to follow the key steps in long-term financial planning that lead to financial security and peace of mind.

Why Long-Term Financial Planning Matters

Taking the time to understand the steps in long-term financial planning isn’t just smart—it’s essential. A well-thought-out plan gives you control, clarity, and confidence as you navigate life’s financial twists and turns. Here’s why long-term planning truly matters:

Financial Stability: It helps you prepare for major life events like retirement, education costs, or homeownership—without last-minute panic.

Smarter Decision-Making: You’re more likely to make informed, strategic choices rather than emotional or impulsive ones.

Wealth Building: Following the right steps in long-term financial planning allows your money to grow through smart saving and investing.

Emergency Readiness: With a long-term plan in place, you’re better equipped to handle job loss, health issues, or market downturns.

Peace of Mind: Simply put, knowing you’re working toward your future reduces stress and brings confidence to your daily life.

When you commit to the right financial planning steps, you’re not just preparing for the future—you’re shaping it on your terms.

Key Steps in Long-Term Financial Planning

Getting your financial future on track starts with structure—and that’s where the steps in long-term financial planning come in. By following a clear, step-by-step approach, you’ll create a plan that adapts to life changes and helps you build lasting security. Let’s explore each step in detail:

1. Define Your Vision and Long-Term Goals

Every plan begins with a purpose.

Identify common goals like retirement, children’s education, or owning property.

Make each goal specific, measurable, and time-bound—for example, “Retire at 60 with $1 million in savings.”

2. Assess Your Current Financial Situation

You can’t move forward if you don’t know where you stand.

Evaluate your income, current savings, outstanding debts, and investments.

This creates your financial baseline, helping you spot strengths, gaps, and opportunities.

3. Estimate Future Needs and Expenses

Planning long-term means anticipating future costs.

Use retirement calculators, education cost estimates, and inflation projections to build realistic expectations.

Factor in your desired lifestyle, not just minimum survival needs.

4. Develop a Saving and Investment Strategy

Now it’s time to grow your wealth with intention.

Select the right mix of investment vehicles like mutual funds, stocks, or retirement accounts.

Balance risk and return based on your timeline—longer horizons can usually handle more risk.

5. Plan for Risk and Insurance Coverage

Protecting what you’ve built is just as important as growing it.

Ensure you have the right health, life, and disability insurance for your situation.

A good insurance strategy provides financial security against life’s unexpected events.

6. Create a Tax-Efficient Plan

Taxes can eat into your gains—unless you plan ahead.

Explore long-term tax strategies, such as capital gains management or charitable contributions.

Leverage retirement accounts and legal structures like trusts to optimize your tax position.

7. Review, Monitor, and Adjust Regularly

A financial plan isn’t static—it’s a living document.

Schedule annual reviews or updates after major life events (job change, marriage, new child).

Adjust your plan as income, expenses, and market conditions evolve.

By following these steps in long-term financial planning, you’ll build a strategy that’s not only smart—but sustainable for the life you’re working hard to create.

Read Also : Financial Planning Cycle: What It Is and Why It Matters in Today’s Economy

Mistakes to Avoid in Long-Term Planning

Even if you follow the right steps in long-term financial planning, a few common mistakes can still derail your progress. Being aware of these pitfalls helps you stay on track and make smarter decisions over time. Here are the most frequent mistakes—and how to avoid them:

Not Setting Clear Goals: Vague objectives lead to vague outcomes. Define specific, time-bound goals to guide your strategy.

Ignoring Inflation: Over decades, inflation can drastically reduce your purchasing power. Always factor it into your future cost estimates.

Underestimating Life Changes: Marriage, children, health issues, or career shifts can all impact your plan—so build in flexibility.

Focusing Only on Saving, Not Investing: Saving alone rarely beats inflation. Investing is essential to grow wealth over the long term.

Failing to Review Your Plan: A “set it and forget it” approach doesn’t work. Review your plan regularly to adjust for new goals or changes.

Avoiding these mistakes is just as important as following the correct steps in long-term financial planning—and can make the difference between drifting and achieving real financial security.

Read Also : Accounting and Finance for Managers: Essential Knowledge for Business Success

How Training Can Strengthen Your Long-Term Financial Skills

If you’re serious about mastering the steps in long-term financial planning, structured training can make a huge difference. Financial education gives you the tools, mindset, and confidence to make smarter decisions for the future. Here’s how training can help:

Clarifies Core Concepts: Training helps you fully understand budgeting, investing, risk management, and retirement planning.

Teaches Practical Tools: Learn how to use financial calculators, investment platforms, and tax planning apps effectively.

Improves Decision-Making: With expert insights, you’ll be able to assess options and avoid common financial mistakes.

Encourages Long-Term Thinking: Training shifts your mindset from short-term spending to long-term wealth building.

Boosts Confidence: The more you learn, the more confident you’ll feel in applying the steps in long-term financial planning to your personal or professional life.

Whether you’re just starting or refining your strategy, training turns guesswork into action—and knowledge into real results.

Read Also :The Ultimate Guide to Choosing the Best Finance Course for Career Success

Who Should Start Long-Term Financial Planning?

The truth is, anyone with financial goals can benefit from learning and applying the steps in long-term financial planning. Whether you’re just starting out or already mid-career, long-term planning helps you take control of your future. Here’s who should seriously consider starting now:

Young Professionals: The earlier you start, the more you benefit from compounding and smart goal-setting.

Families and Parents: Long-term planning helps prepare for education costs, homeownership, and family protection.

Freelancers and Business Owners: With unpredictable income, long-term planning offers structure and security.

Mid-Career Professionals: It’s the perfect time to assess retirement readiness and fine-tune financial strategies.

Anyone Nearing Retirement: Planning ahead ensures a smoother transition and better control over retirement income.

No matter your life stage, starting the steps in long-term financial planning today gives you more options and fewer regrets tomorrow.

Read Also : Financial Planning for an Individual: How to Build a Secure and Prosperous Future

Conclusion: Start Planning Today for the Life You Want Tomorrow

Taking action on the steps in long-term financial planning is one of the most empowering decisions you can make. From defining your goals and assessing your financial position to creating an investment strategy and reviewing your plan regularly, each step builds a foundation for lasting security and peace of mind.

The key is to start early and stay consistent. Your financial future doesn’t depend on how much you have today—it depends on the steps you take now to shape the life you want tomorrow.

Ready to secure your future? Enroll in our expert-led long-term financial planning course now!

LBTA is a globally recognized platform offering specialized programs designed to elevate both individual and corporate capabilities. Our services include:

General Training Programs in areas like finance, management, marketing, engineering, and human resources

Customized Training to address the specific challenges and goals of your organization

Research and Consulting services to help businesses optimize performance and make informed decisions

In-House Training delivered directly to your team, wherever you are

With active training centers in London, Dubai, Istanbul, Kuala Lumpur, and other global hubs, LBTA is your trusted partner in mastering the steps in long-term financial planning—and turning knowledge into lasting impact.

Read Also : How to Start Working Towards Personal Financial Planning: A Beginner’s Guide to Financial Freedom

FAQs

1. What are the key steps in long-term financial planning?

They include setting long-term goals, assessing your current finances, estimating future needs, creating an investment strategy, and reviewing your plan regularly.

2. When should I start long-term financial planning?

The best time to start is now—starting early gives you more time to grow your savings and prepare for future financial goals.

3. How often should I update my financial plan?

At least once a year, or whenever there are major life changes like a new job, marriage, or the birth of a child.

4. Do I need a financial advisor for long-term planning?

Not necessarily, but working with an advisor can provide personalized guidance, help avoid mistakes, and optimize your financial strategy.

5. What’s the difference between short-term and long-term financial planning?

Short-term planning focuses on immediate needs (0–3 years), while long-term planning targets goals 5 years or more into the future, like retirement or education.

What Is Personal Financial Planning?

Before diving into how to start working towards personal financial planning, it’s important to understand what it actually means. Personal financial planning is the process of managing your money to achieve specific life goals. It’s not just about saving—it’s about creating a strategy that works for your lifestyle. Here’s what it typically includes:

Setting Financial Goals: Identifying what you want to achieve financially—whether short-term (like paying off a credit card) or long-term (like buying a house or retiring).

Budgeting: Creating a plan for how you’ll earn, spend, and save money each month.

Managing Debt: Understanding your liabilities and using strategies to pay off loans efficiently.

Saving and Investing: Building an emergency fund, saving for big purchases, and growing wealth through investments.

Planning for the Future: Preparing for major life events such as education, marriage, or retirement with a clear roadmap.

Understanding these components is the first step in how to start working towards personal financial planning that truly supports your life and goals.

Read Also : Financial Planning for an Individual: How to Build a Secure and Prosperous Future

Why You Should Start Personal Financial Planning Today

If you’re asking yourself how to start working towards personal financial planning, the answer is simple—start now. The earlier you begin, the more control you have over your money, goals, and peace of mind. Here’s why taking action today makes a real difference:

Time Is Your Best Asset: The sooner you start, the more time you have to save, invest, and benefit from compound growth.

Reduces Financial Stress: Planning gives you a clearer picture of your finances, which helps you feel more in control and less anxious.

Prepares You for the Unexpected: Life is full of surprises—having a plan means you’re better equipped to handle emergencies or job changes.

Improves Your Spending Habits: When you plan, you become more intentional with your money and avoid unnecessary expenses.

Brings You Closer to Your Goals: Whether it’s buying a car, starting a business, or traveling the world, planning brings your goals within reach.

Learning how to start working towards personal financial planning today gives you a head start on a financially stable and secure tomorrow.

Read Also :The Ultimate Guide to Choosing the Best Finance Course for Career Success

Step-by-Step: How to Start Working Towards Personal Financial Planning

If you’re serious about gaining control of your money, this guide will walk you through exactly how to start working towards personal financial planning—one simple, practical step at a time. No jargon. No overwhelm. Just clear action.

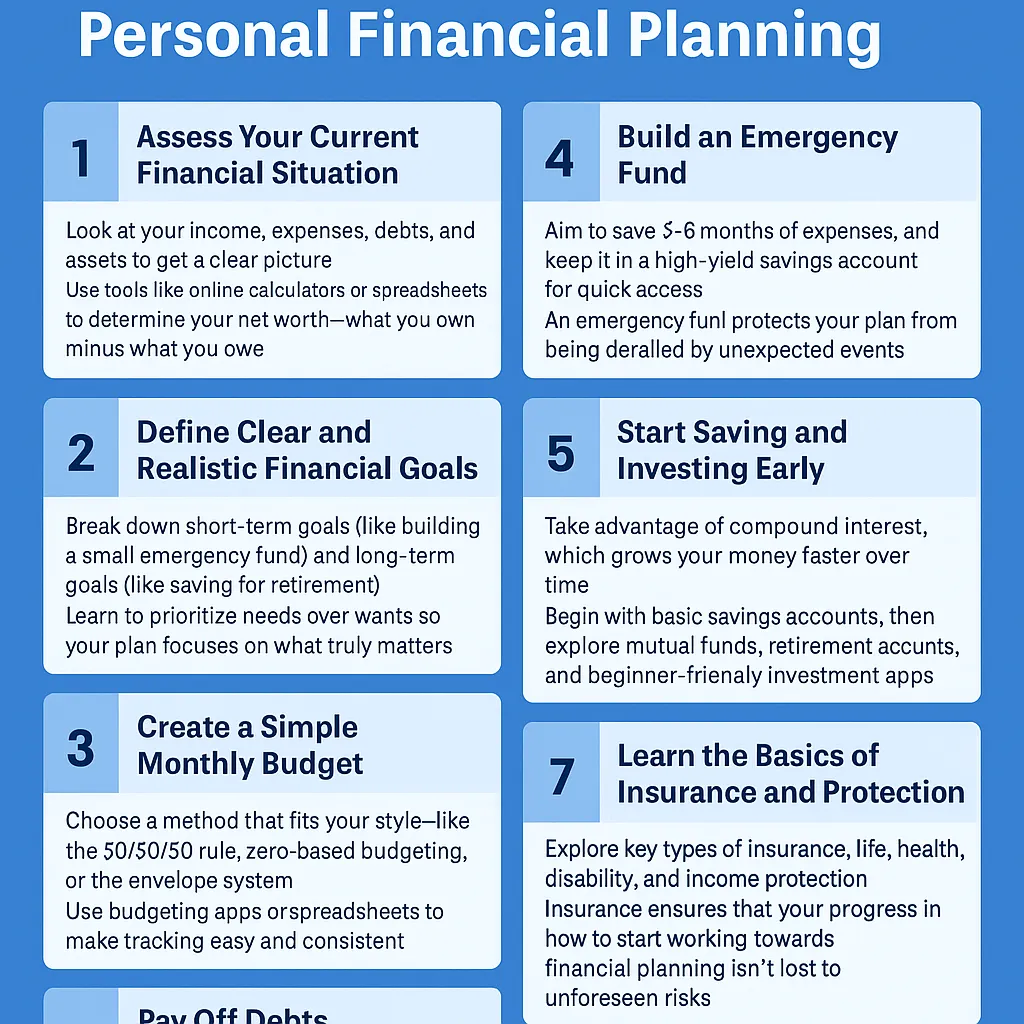

1. Assess Your Current Financial Situation

The first step in how to start working towards personal financial planning is understanding where you stand financially.

Look at your income, expenses, debts, and assets to get a clear picture.

Use tools like online calculators or spreadsheets to determine your net worth—what you own minus what you owe.

2. Define Clear and Realistic Financial Goals

Next, clarify what you’re working toward.

Break down short-term goals (like building a small emergency fund) and long-term goals (like saving for retirement).

Learn to prioritize needs over wants so your plan focuses on what truly matters.

3. Create a Simple Monthly Budget

A budget is your financial roadmap.

Choose a method that fits your style—like the 50/30/20 rule, zero-based budgeting, or the envelope system.

Use budgeting apps or spreadsheets to make tracking easy and consistent.

4. Build an Emergency Fund

This is one of the most important steps in how to start working towards personal financial planning.

Aim to save 3–6 months of expenses, and keep it in a high-yield savings account for quick access.

An emergency fund protects your plan from being derailed by unexpected events.

5. Start Saving and Investing Early

You don’t need a lot to get started—you just need to start.

Take advantage of compound interest, which grows your money faster over time.

Begin with basic savings accounts, then explore mutual funds, retirement accounts, and beginner-friendly investment apps.

6. Pay Off Debts Strategically

Debt can slow down your progress if left unchecked.

Focus on high-interest debts first by understanding interest rates and repayment terms.

Consider strategies like the avalanche (highest interest first) or snowball (smallest balance first) methods.

7. Learn the Basics of Insurance and Protection

No financial plan is complete without protection.

Explore key types of insurance: life, health, disability, and income protection.

Insurance ensures that your progress in how to start working towards personal financial planning isn’t lost to unforeseen risks.

8. Review, Monitor, and Adjust

A financial plan is not a one-time document—it evolves.

Set monthly, quarterly, or annual review dates to track your progress.

Make changes as life evolves—new job, marriage, kids, or new goals.

Following these steps is the most practical way to succeed in how to start working towards personal financial planning—one action, one habit, one goal at a time.

Common Roadblocks and How to Overcome Them

Many people want to improve their finances but get stuck along the way. Understanding the most common obstacles—and how to deal with them—can make a big difference as you figure out how to start working towards personal financial planning. Here are some roadblocks to watch out for:

Lack of Knowledge: Not knowing where to begin can feel overwhelming. Start with basic resources or take a beginner-friendly course to build confidence.

Inconsistent Habits: Skipping budgets or ignoring spending limits disrupts your progress. Build small, daily habits that are easy to maintain.

Emotional Spending: Shopping under stress or boredom can sabotage goals. Track emotional triggers and set spending limits in advance.

Living Paycheck to Paycheck: With no room to save, it’s hard to plan ahead. Start by trimming unnecessary expenses and automating small savings.

Fear of Facing Reality: Avoiding your financial situation won’t make it better. Facing your numbers honestly is a bold first step in how to start working towards personal financial planning.

By recognizing these challenges early, you’ll be better equipped to stay motivated and make steady progress.

Read Also : Accounting and Finance for Managers: Essential Knowledge for Business Success

Why Take a Course on Personal Financial Planning?

If you’re unsure how to start working towards personal financial planning, taking a course can give you the structure, clarity, and confidence you need. It’s one of the smartest investments you can make—whether you’re just starting out or trying to fix past mistakes. Here’s why it’s worth it:

Guided Learning: A course walks you through each step in order, so you don’t feel lost or overwhelmed.

Practical Tools: You’ll learn how to use budgeting apps, investment calculators, and planning worksheets that make managing money easier.

Expert Advice: Courses are often taught by professionals who share real-world tips, not just textbook theory.

Accountability: Being in a structured environment motivates you to take action and follow through.

Long-Term Value: The skills you gain from learning how to start working towards personal financial planning will benefit you for the rest of your life.

Whether online or in-person, a course can help you stop guessing—and start building a financial future with purpose.

Read Also : Stages of Financial Planning Process: A Step-by-Step Guide to Smart Financial Management

Who Should Start Planning Now?

The truth is, there’s no “perfect time” to begin—everyone benefits from taking that first step. If you’re wondering how to start working towards personal financial planning, the answer is simple: start now, no matter your age or income. Here’s who should seriously consider getting started today:

Young Adults: Starting early builds strong money habits and allows compound interest to work in your favor.

New Graduates: Planning helps manage student loans, start saving, and avoid early financial mistakes.

Mid-Career Professionals: It’s the ideal time to fine-tune your goals, increase investments, and protect your family’s future.

Freelancers and Business Owners: Planning helps smooth out irregular income and ensures you’re covered during slow months.

Anyone Feeling Financially Uncertain: If you’re unsure where your money goes each month, it’s time to build a plan and take control.

No matter your starting point, learning how to start working towards personal financial planning now sets the foundation for financial peace of mind later.

Conclusion: Take the First Step Toward Financial Confidence

Now that you know how to start working towards personal financial planning, it’s time to take action. From assessing your current financial situation to setting goals, building a budget, saving, investing, and reviewing your progress—every step you take brings you closer to a future with less stress and more control.

You don’t need to have everything figured out today. What matters most is starting. The earlier you begin planning, the stronger your financial foundation will be—no matter your income or life stage.

Ready to start your journey? Join our personal financial planning course today!

LBTA is a global professional development provider offering a wide range of specialized programs designed to help individuals and organizations thrive. Our services include:

General Training Programs across finance, management, marketing, engineering, and HR

Customized Training built specifically around your goals and industry needs

Research and Consulting to support performance improvement and decision-making

In-House Training brought directly to your team, anywhere in the world

With locations in London, Dubai, Istanbul, Kuala Lumpur, and beyond, LBTA is your trusted partner in building real financial confidence—for life and for work.

Read Also : Financial Planning Cycle: What It Is and Why It Matters in Today’s Economy

FAQs

1. What is personal financial planning?

It’s the process of setting financial goals and creating a strategy to manage income, expenses, savings, and investments to achieve those goals.

2. How do I start working towards personal financial planning?

Begin by assessing your current finances, setting realistic goals, creating a monthly budget, and building an emergency fund.

3. Do I need a high income to start financial planning?

No. You can start at any income level. The key is to manage what you have wisely and build habits that support your goals.

4. How often should I review my financial plan?

At least once a year—or whenever a major life change occurs, like a new job, marriage, or having a child.

5. Can a financial planning course really help?

Yes. It provides structure, expert guidance, and practical tools to help you plan effectively and avoid common financial mistakes.

Quick Summary

- Understand the importance of financial planning.

- Learn key steps to create a personal financial plan.

- Avoid common mistakes and enhance decision-making.

Quick Summary

- Financial planning is essential for achieving personal financial goals.

- A structured approach helps in managing income, expenses, and investments.

- Regular monitoring and adjustments are key to staying on track.

What Is Financial Planning for an Individual?

Financial planning for an individual involves creating a comprehensive strategy to manage one’s finances effectively. This includes assessing current financial situations, setting future financial goals, and developing a roadmap to achieve those goals. It encompasses various aspects such as budgeting, saving, investing, and risk management. The ultimate aim is to ensure financial stability and growth over time.

Why Every Individual Needs a Financial Plan

Having a financial plan is crucial for several reasons:

- Goal Achievement: A financial plan helps individuals set and prioritize their financial goals, whether it’s buying a home, funding education, or planning for retirement.

- Financial Security: It provides a framework for managing risks and uncertainties, ensuring that individuals are prepared for unexpected expenses or economic downturns.

- Informed Decision-Making: A well-structured financial plan enables individuals to make informed decisions regarding investments, savings, and expenditures.

- Peace of Mind: Knowing that there is a plan in place can reduce stress and anxiety related to financial matters.

The Key Steps of Financial Planning for an Individual

Creating a financial plan involves several key steps:

1. Set Clear Financial Goals

Setting clear, measurable, and achievable financial goals is the first step in financial planning. Goals can be short-term (e.g., saving for a vacation) or long-term (e.g., retirement savings). It’s essential to define these goals in specific terms:

- Short-term goals: Saving for a new car, paying off credit card debt.

- Medium-term goals: Saving for a home down payment, funding a child’s education.

- Long-term goals: Retirement savings, estate planning.

2. Track Income and Expenses

Understanding where your money comes from and where it goes is vital for effective financial planning. Tracking income and expenses helps individuals:

- Identify spending patterns.

- Recognize areas where they can cut back.

- Ensure they are living within their means.

Using budgeting tools or apps can simplify this process, making it easier to visualize financial health.

3. Create a Savings and Investment Strategy

A robust savings and investment strategy is essential for building wealth over time. This includes:

- Emergency Fund: Setting aside 3-6 months’ worth of living expenses for unexpected situations.

- Retirement Accounts: Contributing to retirement accounts like 401(k)s or IRAs to take advantage of tax benefits.

- Investment Portfolio: Diversifying investments across stocks, bonds, and other assets to balance risk and return.

4. Manage Debts Wisely

Debt management is a critical component of financial planning. Individuals should:

- Prioritize paying off high-interest debts first.

- Consider debt consolidation options if applicable.

- Avoid accumulating unnecessary debt by living within their means.

5. Plan for Insurance and Risk Management

Insurance is a vital part of financial planning, protecting individuals from unforeseen events. Key types of insurance to consider include:

- Health Insurance: To cover medical expenses.

- Life Insurance: To provide for dependents in case of untimely death.

- Disability Insurance: To protect income in case of illness or injury.

6. Monitor and Adjust the Plan Regularly

Financial planning is not a one-time event; it requires ongoing monitoring and adjustments. Individuals should:

- Review their financial plan at least annually.

- Adjust goals and strategies based on life changes (e.g., marriage, children, job changes).

- Stay informed about market trends and economic changes that may impact their financial situation.

Common Mistakes in Personal Financial Planning

Even with the best intentions, individuals often make mistakes in their financial planning. Common pitfalls include:

- Neglecting to Set Goals: Without clear goals, it’s challenging to create a focused financial plan.

- Ignoring Debt: Failing to address debt can hinder financial progress.

- Lack of Diversification: Putting all investments in one area increases risk.

- Not Reviewing Regularly: Failing to adjust the plan can lead to missed opportunities or increased risks.

How Training Can Improve Personal Financial Decision-Making

Investing in financial education can significantly enhance personal financial decision-making. Training programs can provide:

- Knowledge of Financial Concepts: Understanding key financial principles helps individuals make informed choices.

- Practical Skills: Learning how to create budgets, analyze investments, and manage debts effectively.

- Confidence: Gaining knowledge can empower individuals to take control of their financial futures.

Who Should Take a Financial Planning Course?

Financial planning courses are beneficial for:

- Young Professionals: Starting their financial journey and needing guidance.

- Families: Looking to manage household finances and plan for children’s education.

- Individuals Approaching Retirement: Seeking to optimize their retirement savings and income.

- Anyone Seeking Financial Literacy: Those who want to improve their understanding of personal finance.

Conclusion: Your Financial Future Starts with a Plan

In conclusion, mastering financial planning is essential for individuals looking to secure their financial future in 2026 and beyond. By setting clear goals, tracking finances, and continuously adjusting your plan, you can navigate the complexities of personal finance with confidence.

| Feature | Option A | Option B |

|---|---|---|

| Comprehensive Coverage | Yes | No |

| Personalized Strategy | Yes | Limited |

| Ongoing Support | Yes | No |

Comparison of key aspects.

Elevate Your Financial Knowledge with LBTA

At LBTA, we understand the importance of financial literacy in today’s world. Our comprehensive courses are designed to equip you with the knowledge and skills necessary to make informed financial decisions. Whether you are just starting your financial journey or looking to enhance your existing knowledge, our expert-led training can help you achieve your financial goals.

Frequently Asked Questions (FAQ)

Q: What is financial planning for individuals?

Q: Why is financial planning important for individuals?

Q: What are the key components of a financial plan?

Q: How can I start my financial planning journey?

Q: What tools can assist with financial planning for individuals?

Q: How often should I review my financial plan?

Quick Summary

- Understand the stages of the financial planning cycle.

- Learn the importance of structured financial planning.

- Discover how professional training can enhance your skills.

What Is the Financial Planning Cycle?

The financial planning cycle is a systematic process that helps individuals and organizations manage their finances effectively. It involves a series of steps that guide the planning, execution, and evaluation of financial strategies. The cycle is iterative, meaning that it is designed to be repeated as circumstances change and new goals are set. This approach ensures that financial plans remain relevant and effective over time.

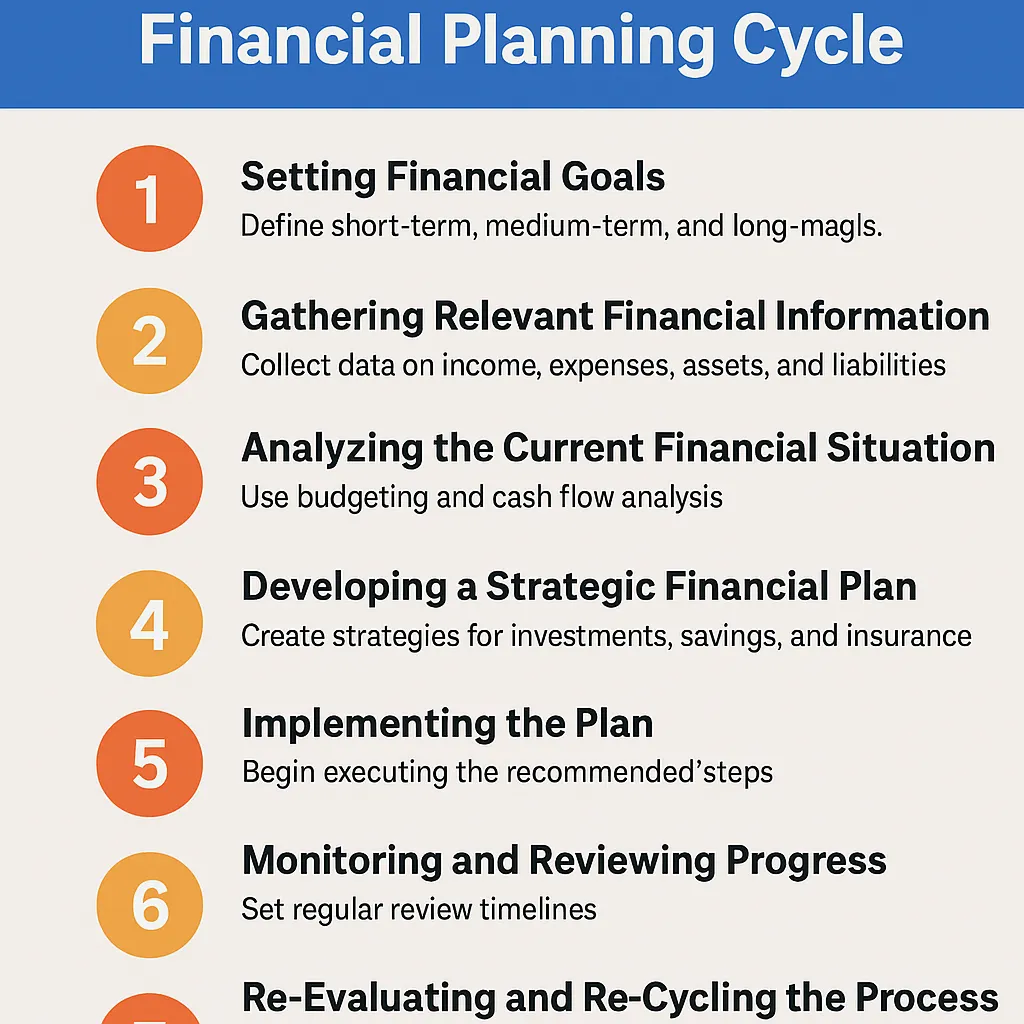

The financial planning cycle typically includes the following stages:

* Setting financial goals

* Gathering relevant financial information

* Analyzing the current financial situation

* Developing a strategic financial plan

* Implementing the plan

* Monitoring and reviewing progress

* Re-evaluating and re-cycling the process

Why Understanding the Financial Planning Cycle Is Crucial

Understanding the financial planning cycle is essential for several reasons:

* Adaptability: In a dynamic economic environment, having a structured approach allows for quick adjustments to financial plans as needed.

* Goal Achievement: A clear cycle helps in setting measurable and achievable financial goals, increasing the likelihood of success.

* Resource Allocation: It aids in the efficient allocation of resources, ensuring that funds are directed towards the most impactful areas.

* Risk Management: By continuously monitoring and reviewing financial plans, potential risks can be identified and mitigated early.

The Main Stages of the Financial Planning Cycle

1. Setting Financial Goals

Setting financial goals is the foundation of the financial planning cycle. Goals should be SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. For instance, instead of saying, “I want to save money,” a SMART goal would be, “I want to save $10,000 for a home down payment within the next two years.” This clarity helps in formulating a focused financial strategy.

2. Gathering Relevant Financial Information

This stage involves collecting all necessary financial data, including income, expenses, assets, and liabilities. Tools like budgeting apps or financial spreadsheets can be beneficial in organizing this information. The more accurate and comprehensive the data, the better the analysis and planning will be.

3. Analyzing the Current Financial Situation

Once the data is gathered, the next step is to analyze it to understand the current financial position. This includes assessing cash flow, net worth, and debt levels. Financial ratios, such as the debt-to-income ratio, can provide insights into financial health. For example, a high debt-to-income ratio may indicate the need for debt reduction strategies.

4. Developing a Strategic Financial Plan

With a clear understanding of the current situation, the next step is to develop a strategic financial plan. This plan should outline how to achieve the set goals, including investment strategies, savings plans, and debt management. It’s essential to consider various scenarios and potential obstacles that may arise.

5. Implementing the Plan

Implementation is where the theoretical aspects of the financial plan become practical. This may involve setting up automatic transfers to savings accounts, investing in stocks or bonds, or adjusting spending habits. Effective implementation requires discipline and commitment to the plan.

6. Monitoring and Reviewing Progress

Regularly monitoring progress is crucial to ensure that the financial plan remains on track. This could involve monthly budget reviews or quarterly financial check-ins. Adjustments may be necessary based on changes in income, expenses, or financial goals.

7. Re-Evaluating and Re-Cycling the Process

The financial planning cycle is not a one-time event; it is an ongoing process. As life circumstances change—such as a new job, marriage, or retirement—financial goals may need to be re-evaluated. This stage involves revisiting the initial steps and making necessary adjustments to the financial plan.

Benefits of Following a Structured Financial Planning Cycle

- Clarity and Focus: A structured approach provides clarity on financial goals and the steps needed to achieve them.

- Improved Financial Health: Regular monitoring and adjustments can lead to better financial health and stability.

- Informed Decision-Making: A comprehensive understanding of one’s financial situation enables better decision-making regarding investments and expenditures.

- Long-Term Success: A continuous cycle of planning and re-evaluation fosters long-term financial success and security.

Common Pitfalls in Financial Planning Cycles (And How to Avoid Them)

While the financial planning cycle is a powerful tool, there are common pitfalls that can hinder success:

* Lack of Specificity: Vague goals can lead to unfocused planning. Ensure that all goals are specific and measurable.

* Ignoring Changes: Failing to adjust the plan in response to life changes can derail progress. Regular reviews are essential.

* Overcomplicating the Process: Keeping the planning process simple and straightforward can enhance adherence and effectiveness.

* Neglecting Professional Advice: Sometimes, seeking help from financial advisors can provide valuable insights and guidance.

How Professional Training Enhances Financial Planning Skills

Professional training in financial planning can significantly enhance one’s ability to navigate the financial planning cycle. Training programs often cover:

* Advanced Financial Concepts: Understanding complex financial instruments and strategies.

* Regulatory Knowledge: Staying updated on financial regulations and compliance requirements.

* Practical Applications: Learning through case studies and real-world scenarios to apply theoretical knowledge.

* Networking Opportunities: Connecting with other professionals in the field can provide support and resources.

Who Should Master the Financial Planning Cycle?

Mastering the financial planning cycle is beneficial for:

* Individuals: Anyone looking to improve their personal financial situation.

* Small Business Owners: Entrepreneurs who need to manage business finances effectively.

* Financial Advisors: Professionals seeking to enhance their service offerings to clients.

* Students: Those pursuing careers in finance or business management.

| Feature | Option A | Option B |

|---|---|---|

| Comprehensive Training | Yes | No |

| Practical Applications | High | Low |

| Expert Guidance | Available | Limited |

Comparison of key aspects.

Conclusion: Make Financial Planning a Repeatable Success

In conclusion, the financial planning cycle is an invaluable framework for achieving financial success. By understanding and implementing each stage of the cycle, individuals and businesses can navigate the complexities of financial management with confidence. Whether you are just starting your financial journey or looking to refine your existing strategies, embracing this cycle will lead to informed decisions and sustainable growth.

Frequently Asked Questions (FAQ)

Q: What is the Financial Planning Cycle?

Q: Why is the Financial Planning Cycle important?

Q: How often should I review my financial plan?

Q: Can the Financial Planning Cycle be used for both individuals and businesses?

Q: Do I need a financial advisor to go through the cycle?

Q: What are some common pitfalls in financial planning?

What Is Financial Planning and Why It Matters

Financial planning is the structured process of setting goals, assessing your financial situation, and creating a strategy to achieve lasting financial health. At the core of this approach are the stages of the financial planning process, which guide individuals and businesses from uncertainty to clarity. Here’s why it matters:

Goal Clarity: Financial planning helps you define short- and long-term goals—whether that’s buying a home, saving for education, or retiring comfortably.

Informed Decisions: With a structured process, you can make smarter choices around spending, saving, investing, and risk management.

Proactive Problem-Solving: Planning prepares you for life’s uncertainties, from market shifts to personal emergencies.

Long-Term Stability: By following the stages of the financial planning process, you stay focused, consistent, and confident in your financial journey.

In short, financial planning isn’t just about money—it’s about building a secure and purposeful future.

Overview of the Financial Planning Process

The journey to financial success is rarely a straight line—but with the right steps, it becomes much easier to navigate. The stages of the financial planning process provide a structured approach that helps individuals and businesses set goals, track progress, and adjust along the way. Typically, the process includes:

Establishing the Relationship – Setting expectations and defining the scope of the financial planning engagement.

Gathering Financial Data – Collecting details about income, expenses, assets, liabilities, and personal goals.

Analyzing the Information – Evaluating the current financial situation to identify strengths, weaknesses, and opportunities.

Developing Recommendations – Crafting a customized financial plan based on your needs, goals, and timeline.

Implementing the Plan – Putting the strategy into action through investments, budgeting, insurance, and other tools.

Monitoring and Updating – Reviewing and adjusting the plan regularly to stay on track and adapt to changes.

Understanding these stages of the financial planning process ensures you’re not just reacting to life—you’re leading it with intention.

Read Also : Accounting and Finance for Managers: Essential Knowledge for Business Success

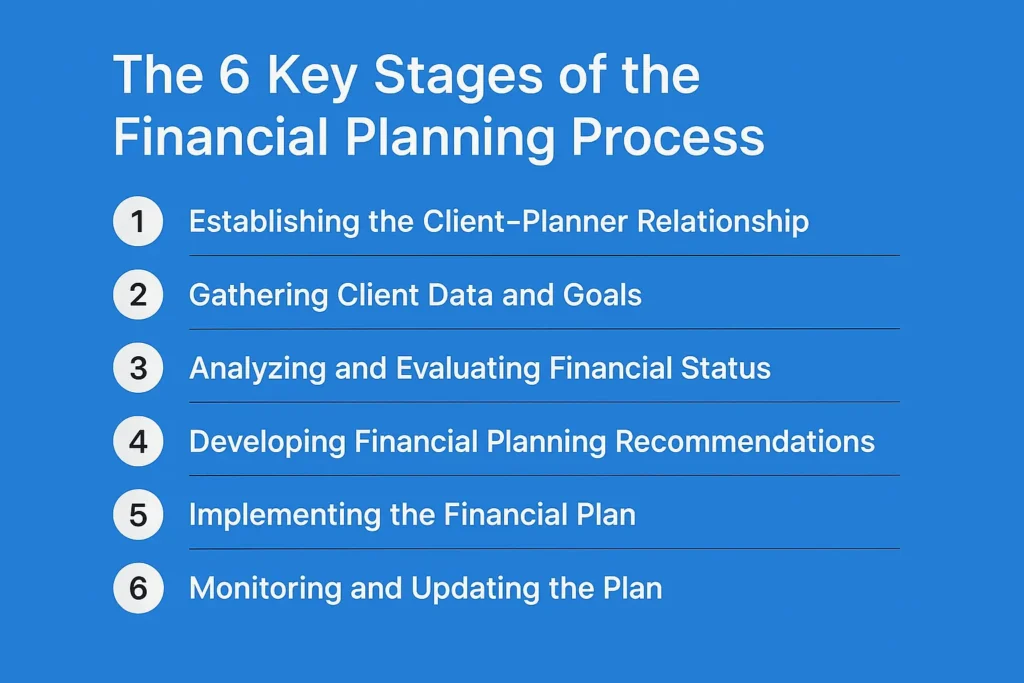

The 6 Key Stages of the Financial Planning Process

Financial planning isn’t a one-time task—it’s an ongoing journey. By understanding the stages of the financial planning process, individuals and businesses can make more informed decisions, stay focused on their goals, and adjust their course as life changes. Let’s explore each of the six key stages:

1. Establishing the Client–Planner Relationship

The first step in the stages of the financial planning process is all about trust and clarity.

Clarifying roles and responsibilities ensures both the planner and the client know what to expect from each other.

Setting communication expectations lays the foundation for a transparent, collaborative relationship.

2. Gathering Client Data and Goals

Good planning starts with good information.

Identifying financial objectives—like retirement, homeownership, or debt reduction—helps set the direction.

Collecting quantitative and qualitative data provides the planner with a complete picture of the client’s current situation.

3. Analyzing and Evaluating Financial Status

Now it’s time to crunch the numbers and look at the big picture.

Reviewing assets, liabilities, income, and expenses helps determine financial strengths and weaknesses.

Identifying gaps and opportunities allows for smarter strategy development and risk management.

4. Developing Financial Planning Recommendations

This stage turns insights into action.

Creating a tailored action plan ensures the client’s goals are addressed with clear, actionable steps.

Considering alternatives and trade-offs provides flexibility while keeping the strategy aligned with personal values.

5. Implementing the Financial Plan

Strategy means little without execution.

Coordinating with other professionals like tax advisors, insurance agents, or estate planners ensures the plan is comprehensive.

Assigning tasks and setting timelines helps bring the financial plan to life in a structured, realistic way.

6. Monitoring and Updating the Plan

The final (and ongoing) phase in the stages of the financial planning process is keeping the plan relevant.

Reviewing progress and adapting to life or market changes ensures the strategy evolves with the client’s needs.

Continuous improvement and recalibration help maintain alignment with long-term goals.

When all six stages are followed thoughtfully, financial planning becomes more than a service—it becomes a lifelong advantage.

Read Also :The Ultimate Guide to Choosing the Best Finance Course for Career Success

Common Mistakes to Avoid During the Financial Planning Process

Even with the best intentions, many people stumble along the stages of the financial planning process—and those mistakes can cost time, money, and peace of mind. Being aware of these common pitfalls can help you plan smarter and avoid costly setbacks:

Skipping Goal-Setting: Jumping into numbers without clearly defining your financial goals can lead to a plan that lacks direction and purpose.

Inaccurate or Incomplete Data: Providing outdated or partial financial information leads to poor analysis and unrealistic recommendations.

Failing to Revisit the Plan: A plan that isn’t reviewed regularly can quickly become irrelevant as your life or the market changes.

Overlooking Risk Management: Not accounting for insurance, emergency funds, or potential setbacks leaves you vulnerable in a crisis.

Trying to Do Everything Alone: Financial planning is complex—working with a professional ensures each stage is handled with care and expertise.

Emotional Decision-Making: Letting fear or excitement override logic can derail even the most well-thought-out plan.

Avoiding these common mistakes allows you to move through the stages of the financial planning process with more confidence, clarity, and long-term success.

Read Also :Essential Accounting Skills Needed for Success: A Comprehensive Guide

Why Training in Financial Planning Is a Game-Changer

Understanding the theory is one thing—applying it with confidence is another. That’s why professional training in financial planning can truly elevate your approach. Whether you’re a finance professional or simply managing your personal wealth, learning the stages of the financial planning process through expert-led training provides powerful advantages:

Structured Knowledge: Training breaks down each stage into clear, practical steps, making complex topics easier to understand and apply.

Real-World Application: Case studies and simulations help you practice what you learn, from goal-setting to risk analysis.

Updated Tools and Insights: Courses teach the latest strategies, software, and compliance standards shaping modern financial planning.

Greater Confidence: Knowing how to move through the process—professionally or personally—gives you the confidence to make informed decisions.

Career Advancement: For financial professionals, mastering the stages of the financial planning process through training adds value to your resume and credibility with clients.

Investing in training is more than education—it’s a leap toward smarter planning and long-term financial success.

Read Also :The Ultimate Guide to Choosing the Best Accounting Course for Your Career

Who Should Learn the Financial Planning Process?

The stages of the financial planning process aren’t just for financial advisors—they’re valuable for anyone who wants to take control of their financial future. Whether you’re managing a household budget or guiding corporate investments, understanding this process empowers better decisions. Here’s who can benefit most:

Individuals and Families: From saving for education to planning retirement, anyone with financial goals can benefit from a structured approach.

Young Professionals: Learning the stages early helps build healthy financial habits and long-term wealth.

Entrepreneurs and Business Owners: Financial planning supports smarter budgeting, forecasting, and sustainable business growth.

Finance and Accounting Professionals: Mastering the process enhances career opportunities and client trust.

HR and Compensation Specialists: Understanding financial planning helps in designing effective employee benefits and retirement packages.

Nonprofit Leaders and Trustees: Financial planning ensures proper fund allocation, compliance, and long-term impact.

No matter your role or background, gaining clarity on the stages of the financial planning process equips you with lifelong financial intelligence.

Conclusion: Master the Financial Planning Process and Take Control of Your Future

The stages of the financial planning process—from setting clear goals and analyzing financial data to implementing and adjusting your plan—form a reliable roadmap to financial clarity and long-term success. Whether you’re managing personal wealth or advising others, understanding these stages equips you to make smarter, more strategic decisions.

Financial planning isn’t something you do once—it’s a lifelong journey. The sooner you learn how to navigate it with confidence, the better prepared you’ll be to achieve your goals and overcome financial challenges.

Want to become a financial planning expert? Join our certified training programs today!

LBTA is a global professional development platform offering specialized programs tailored to both individuals and organizations. We provide:

General Training Programs in finance, management, marketing, engineering, and HR

Customized Training built around your unique needs and industry challenges

Research and Consulting to help organizations optimize performance

In-House Training delivered at your location, aligned with your schedule

With training centers in London, Dubai, Istanbul, Kuala Lumpur, and beyond, LBTA is your trusted partner for building expertise in every step of the financial planning journey.

Read Also :Financial Risk Management: A Comprehensive Guide to Protecting Your Finances

FAQs

1. What is the financial planning process?

It’s a structured approach to setting financial goals, analyzing your current situation, creating a plan, implementing it, and reviewing it regularly.

2. Why is financial planning important?

It helps individuals and businesses make informed financial decisions, reduce risks, and achieve long-term financial goals.

3. How often should I review my financial plan?

At least once a year or whenever a major life or financial event occurs—like marriage, a new job, or a market shift.

4. Can I create a financial plan without a professional?

Yes, but working with a certified planner ensures accuracy, strategy, and professional insight—especially for complex goals.

5. What is the first step in the financial planning process?

The first step is establishing a relationship with a financial planner, where roles, responsibilities, and expectations are clearly defined.

What Is Accounting and Finance for Managers?

If you’re in a leadership role, you’ve likely faced financial decisions—even without a background in finance. That’s exactly why Accounting and Finance for Managers is so important. This concept refers to the practical financial knowledge that managers need to effectively run teams, allocate resources, and contribute to strategic planning. Here’s what sets it apart:

Managerial Definition: Unlike traditional accounting, which focuses on preparing financial reports, Accounting and Finance for Managers is about interpreting those numbers to make smart business decisions.

Different from Specialist Roles: While accountants focus on compliance and finance teams manage investments or capital structure, managerial finance emphasizes how financial insights guide day-to-day operations and long-term planning.

Crucial for Non-Financial Managers: Even if you’re in HR, marketing, or operations, understanding key financial concepts helps you read budgets, justify spending, and align your work with broader business goals.

In short, Accounting and Finance for Managers equips leaders with the financial confidence they need to influence outcomes and drive results.

Why Every Manager Needs Financial Literacy

Being a great manager isn’t just about leading people—it’s also about understanding the financial impact of your decisions. That’s why Accounting and Finance for Managers is more than a nice-to-have; it’s a must-have skill in any industry. Here’s why financial literacy matters for every manager:

Better Budget Management: Managers who understand finance can plan, allocate, and monitor budgets more effectively—avoiding overspending and underperformance.

Stronger Strategic Thinking: Financially literate leaders make smarter choices because they understand how each decision affects the bottom line.

Improved Communication with Finance Teams: When managers speak the language of finance, collaboration with accountants, analysts, and executives becomes clearer and more productive.

Greater Accountability: Understanding key metrics allows managers to justify expenses, evaluate performance, and lead with data-driven confidence.

Incorporating Accounting and Finance for Managers into your leadership toolbox means you’re not just managing people—you’re managing results.

Read Also :The Ultimate Guide to Choosing the Best Finance Course for Career Success

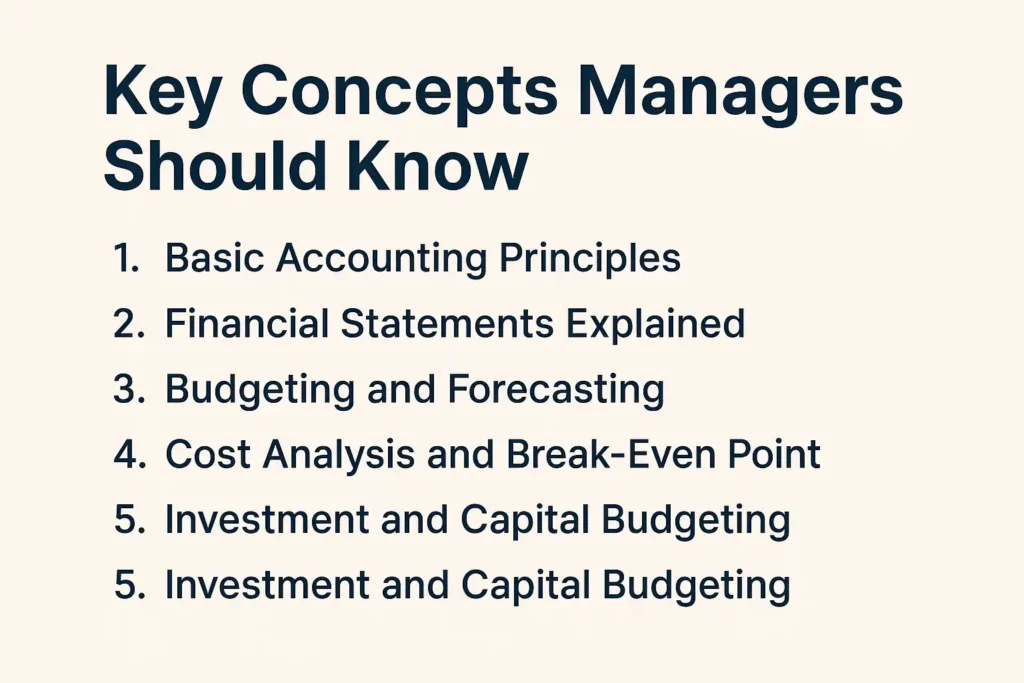

Key Concepts Managers Should Know

Understanding the core principles of finance empowers managers to lead with confidence and clarity. Whether you’re approving budgets, setting goals, or evaluating team performance, these five concepts form the foundation of effective decision-making in Accounting and Finance for Managers.

1. Basic Accounting Principles

At the heart of Accounting and Finance for Managers are the basic building blocks: assets, liabilities, equity, income, and expenses. These elements make up the financial DNA of any business. Managers should also be familiar with the accounting equation (Assets = Liabilities + Equity) and how double-entry bookkeeping ensures every transaction is balanced and accurately recorded. Understanding these fundamentals helps non-financial leaders speak the same language as accountants and make more informed decisions.

2. Financial Statements Explained

Every manager should be able to read and interpret the three primary financial statements:

The balance sheet shows a company’s financial position at a specific point in time.

The income statement reveals profitability over a set period by comparing revenue with expenses.

The cash flow statement tracks the movement of money in and out of the business.

In the context of Accounting and Finance for Managers, knowing how to analyze these reports allows leaders to spot trends, assess performance, and support strategic planning.

3. Budgeting and Forecasting

Budgeting isn’t just about keeping costs under control—it’s a strategic tool for managing resources and measuring progress. Accounting and Finance for Managers emphasizes the importance of comparing planned vs. actual performance, which helps identify gaps, opportunities, and necessary adjustments. Forecasting, on the other hand, enables managers to anticipate future outcomes and make proactive decisions that align with company goals.

4. Cost Analysis and Break-Even Point

Every manager should grasp the difference between fixed and variable costs, as well as how they impact pricing, profit margins, and scalability. In Accounting and Finance for Managers, understanding the break-even point is vital—it’s the moment where total revenue equals total costs, meaning your project or business becomes profitable. This knowledge supports smarter pricing strategies and better resource allocation.

5. Investment and Capital Budgeting

Managers often face choices between competing projects or investments. That’s where tools like Return on Investment (ROI), Payback Period, and Net Present Value (NPV) come into play. Within the scope of Accounting and Finance for Managers, these metrics help leaders evaluate potential returns, assess risk, and select the most value-driven initiatives—ensuring that every dollar invested moves the company forward.

How Accounting and Finance Support Managerial Decision-Making

Good decisions don’t happen by chance—they’re built on the right financial insights. That’s whyAccounting and Finance for Managersplays a vital role in supporting leadership across all departments. Here are some of the ways finance empowers better decision-making:

Budget Evaluation: Managers can assess if projects or departments are operating within budget, helping avoid overspending and improve cost control.

Performance Tracking: By reviewing financial reports, leaders can track progress, spot inefficiencies, and respond proactively to challenges.

Resource Allocation: Financial data helps determine where to invest time, money, and manpower for the greatest return.

Risk Assessment: Accounting tools reveal potential financial risks, enabling managers to plan and act with more caution and foresight.

Strategic Planning: Managers use financial projections and past performance to make informed decisions that align with business goals.

In the context of Accounting and Finance for Managers, these tools are more than just numbers—they’re the foundation for smarter, faster, and more strategic choices.

Read Also :Essential Accounting Skills Needed for Success: A Comprehensive Guide

Common Mistakes Non-Financial Managers Make

Even the most talented leaders can run into trouble when they overlook key financial principles. That’s why Accounting and Finance for Managers is so valuable—it helps prevent common mistakes that can harm performance and profitability. Here are some of the most frequent errors non-financial managers tend to make:

Ignoring Financial Reports: Many managers focus solely on operations, missing out on critical insights hidden in income statements and balance sheets.

Overestimating Budgets: Without financial context, managers may approve budgets that are unrealistic or misaligned with company goals.

Misjudging Profitability: Confusing revenue with profit is a costly mistake—true financial literacy helps managers understand margins and break-even points.

Failing to Monitor Cash Flow: Overlooking cash flow can lead to liquidity issues, even if the business appears profitable on paper.

Making Emotion-Driven Decisions: Without financial data, decisions may be based on instinct rather than facts—leading to poor outcomes.

By applying the principles of Accounting and Finance for Managers, leaders can avoid these pitfalls and lead with both confidence and clarity.

Read Also :The Ultimate Guide to Choosing the Best Accounting Course for Your Career

Learn Accounting and Finance for Managers Through Expert-Led Training

If you’re ready to turn financial understanding into a true leadership skill, Accounting and Finance for Managers training is the next step—and LBTAis here to help.

As a globally recognized platform, LBTA offers expert-led programs that equip professionals with the financial knowledge needed to make smarter, data-driven decisions. From general training in areas like finance, management, and marketing to customized solutions tailored to organizational goals, LBTA ensures every learning experience delivers real impact.

The platform also offers in-house training and consulting services for companies looking to build internal capabilities. With a presence in global business hubs like London, Dubai, Istanbul, and Kuala Lumpur, LBTA makes it easy to access world-class knowledge—wherever you are.

Conclusion: Gain Financial Confidence and Lead with Insight

In today’s results-driven workplace, understanding finance isn’t just for accountants—it’s a leadership skill. By learning the principles of Accounting and Finance for Managers, you’ll gain the confidence to read reports, manage budgets, and make decisions that align with your organization’s goals. Whether you’re leading a small team or managing a major department, financial literacy empowers you to lead with clarity, precision, and impact. Don’t just follow the numbers—understand them, and use them to shape your success.

Read Also :Financial Risk Management: A Comprehensive Guide to Protecting Your Finances

FAQs

What is an accounting and finance manager?

A professional who oversees budgeting, financial reporting, and accounting operations to support business strategy and compliance.

What is management accounting and finance?

It refers to using financial data to assist managers in planning, decision-making, and performance evaluation within an organization.

How do managers use financial accounting?

They use it to understand company performance, control budgets, assess profitability, and make informed strategic decisions.

What is meant by accounting for managers?

It’s the application of accounting principles to help managers interpret financial information and guide business decisions.

Is accounting manager higher than accountant?

Yes, an accounting manager typically supervises accountants and handles higher-level financial oversight and reporting.

Can an accountant be a financial manager?

Yes, with the right experience and skills, an accountant can transition into a financial management role.

Quick Summary

- Understand the importance of financial reporting.

- Learn key principles and common challenges.

- Discover best practices and benefits for professionals.

What Is Financial Reporting and Why It Matters

Financial reporting is the process of producing statements that disclose an organization’s financial status to management, investors, and the government. These reports are crucial for decision-making, as they provide a clear picture of a company’s financial health. Key documents in financial reporting include:

- Balance Sheet

- Income Statement

- Cash Flow Statement

- Statement of Changes in Equity

Understanding financial reporting is essential for several reasons:

- Transparency: It fosters trust among stakeholders by providing a clear view of financial performance.

- Compliance: Adhering to regulations and standards is critical for avoiding legal issues.

- Decision-Making: Accurate reports enable informed decisions that can drive business growth.

Key Principles of Effective Financial Reporting

To ensure that financial reports are effective, certain principles must be adhered to:

- Relevance: Information must be pertinent to the decision-making needs of users.

- Reliability: Reports should be accurate and free from bias.

- Comparability: Financial statements should be consistent over time, allowing for trend analysis.

- Understandability: Reports must be clear and concise, making them accessible to all stakeholders.

These principles help maintain the integrity of financial reporting and ensure that stakeholders can make informed decisions based on the data presented.

Common Challenges in Financial Reporting

Despite its importance, financial reporting comes with several challenges:

- Data Accuracy: Ensuring that all data is accurate and up-to-date can be difficult, especially in large organizations.

- Regulatory Compliance: Keeping up with changing regulations and standards can be overwhelming.

- Timeliness: Producing reports in a timely manner is crucial, yet often challenging due to data collection processes.

- Technology Integration: Many organizations struggle with integrating new technologies into their reporting processes.

Addressing these challenges requires a proactive approach, including investing in technology and training staff to enhance their skills.

Financial Reporting Best Practices You Should Follow

Implementing best practices in financial reporting can significantly enhance the quality and reliability of your reports. Here are some best practices to consider:

- Automate Reporting Processes: Utilize software solutions to streamline data collection and reporting.

- Regular Training: Invest in ongoing training for your finance team to keep them updated on best practices and regulatory changes.

- Implement Internal Controls: Establish robust internal controls to ensure data integrity and compliance.

- Use Dashboards: Create visual dashboards for real-time insights into financial performance.

- Engage Stakeholders: Regularly communicate with stakeholders to understand their reporting needs and expectations.

By following these best practices, organizations can enhance the accuracy and effectiveness of their financial reporting.

Benefits of Following Financial Reporting Best Practices

Adopting best practices in financial reporting offers numerous benefits:

- Improved Decision-Making: Accurate and timely reports lead to better strategic decisions.

- Enhanced Credibility: Reliable financial reports build trust with investors and stakeholders.

- Increased Efficiency: Streamlined processes save time and reduce errors.

- Regulatory Compliance: Staying compliant with regulations minimizes the risk of penalties.

These benefits not only improve the financial health of an organization but also contribute to its overall success.

Learn and Apply Best Practices with Professional Training

To truly excel in financial reporting, professionals should consider enrolling in specialized training programs. LBTA offers comprehensive courses designed to equip finance professionals with the skills and knowledge necessary to implement best practices effectively. Our training covers:

- Advanced financial reporting techniques

- Regulatory compliance updates

- Data analysis and visualization tools

- Real-world case studies and applications

By participating in these training programs, professionals can enhance their expertise and drive their organizations toward financial excellence.

| Feature | Option A | Option B |

|---|---|---|

| Accuracy | High | Medium |

| Timeliness | Real-time | Monthly |

| Compliance | Full | Partial |

Comparison of key aspects.

Conclusion: Turn Financial Reporting Into a Strategic Advantage

In conclusion, mastering financial reporting is essential for professionals looking to make a significant impact in their organizations. By understanding the principles, overcoming challenges, and implementing best practices, you can transform financial reporting from a routine task into a strategic advantage. As we move through 2026, staying informed and skilled in financial reporting will be crucial for success in the competitive business landscape.

Frequently Asked Questions (FAQ)

Q: What are financial reporting best practices?

Q: Why are financial reporting best practices important?

Q: How can professionals implement financial reporting best practices?

Q: What role does technology play in financial reporting best practices?

Q: What are common challenges in adhering to financial reporting best practices?

Q: How often should companies review their financial reporting practices?

What is a Cash Flow Statement?

A Cash Flow Statement in Finance and Accounting is a financial report that tracks the movement of cash into and out of a business over a specific period. It provides a clear picture of a company’s liquidity, showing how well a business generates cash to fund operations, investments, and financial obligations.

Unlike income statements that focus on profitability, Cash Flow Statements in Finance and Accounting highlight a company’s actual cash position, making them essential for financial planning and decision-making.

Key Functions of a Cash Flow Statement in Finance and Accounting

Monitors Liquidity: Ensures a business has enough cash to cover daily expenses.Tracks Cash Inflows and Outflows: Identifies how cash is generated and spent across operations, investments, and financing activities.Supports Financial Decision-Making: Helps businesses plan for expansion, debt repayment, and capital investments.Improves Investor and Lender Confidence: Provides transparency on cash management and financial stability.

Monitors Liquidity: Ensures a business has enough cash to cover daily expenses.Tracks Cash Inflows and Outflows: Identifies how cash is generated and spent across operations, investments, and financing activities.Supports Financial Decision-Making: Helps businesses plan for expansion, debt repayment, and capital investments.Improves Investor and Lender Confidence: Provides transparency on cash management and financial stability.

Cash Flow Statement Formula

A standard Cash Flow Statement in Finance and Accounting follows this formula:

Net Cash Flow = Cash from Operating Activities + Cash from Investing Activities + Cash from Financing Activities

This formula ensures that all cash movements are accounted for, helping businesses maintain a balanced cash position.

Example of a Cash Flow Statement in Finance and Accounting

| Category | Amount ($) |

| Cash Flow from Operations | 50,000 |

| Cash Flow from Investing | (20,000) |

| Cash Flow from Financing | 30,000 |

| Net Cash Flow | 60,000 |

| Beginning Cash Balance | 40,000 |

| Ending Cash Balance | 100,000 |

In this example, the company generated $60,000 in net cash flow, increasing its total cash balance to $100,000.

A well-prepared Cash Flow Statement in Finance and Accounting helps businesses evaluate financial stability, plan for growth, and avoid cash shortages. The next section will explore the key components of a cash flow statement and their significance.

Key Components of a Cash Flow Statement

A Cash Flow Statement in Finance and Accounting consists of three main sections that track different types of cash movements within a business. These components help business owners, investors, and financial analysts understand how cash is generated and used over a specific period.

1. Cash Flow from Operating Activities

Represents cash generated or used in day-to-day business operations. Includes cash receipts from sales, payments to suppliers, employee wages, and tax payments. Positive operating cash flow indicates a company can sustain operations without external financing.

Example Transactions in Cash Flow from Operating Activities:

- Cash received from customers (+ $100,000)

- Salaries and wages paid (- $30,000)

- Rent and utilities paid (- $10,000)

- Taxes paid (- $5,000)

Net Cash from Operating Activities = $100,000 – ($30,000 + $10,000 + $5,000) = $55,000

Why It Matters:

A strong cash flow from operations indicates a business is profitable without relying on external financing.

2. Cash Flow from Investing Activities

Tracks cash spent on or earned from investments in long-term assets. Includes purchase or sale of property, equipment, and securities. Negative cash flow in this section is normal if a company is investing in growth.

Example Transactions in Cash Flow from Investing Activities:

- Purchase of new equipment (- $20,000)

- Sale of an old building (+ $50,000)

Net Cash from Investing Activities = $50,000 – $20,000 = $30,000

Why It Matters:

A company with high capital expenditures may be expanding operations, while a business selling assets may be trying to boost cash reserves.

3. Cash Flow from Financing Activities

Records cash transactions related to debt, equity, and dividends. Includes loan repayments, stock issuance, and dividend payments. Helps assess how a company raises and returns capital to investors and lenders.

Example Transactions in Cash Flow from Financing Activities:

- Loan received from a bank (+ $40,000)

- Loan repayment (- $20,000)

- Dividend payment to shareholders (- $10,000)

Net Cash from Financing Activities = ($40,000) – ($20,000 + $10,000) = $10,000

Why It Matters:

A business that frequently raises money from loans or investors may have higher financial risk, while consistent dividend payments indicate strong profitability.

4. Net Cash Flow and Ending Cash Balance

Net Cash Flow = Operating Cash Flow + Investing Cash Flow + Financing Cash Flow. The ending cash balance shows the total cash available at the end of the reporting period.

Example Calculation:

- Cash Flow from Operating Activities = $55,000

- Cash Flow from Investing Activities = $30,000

- Cash Flow from Financing Activities = $10,000

- Net Cash Flow = $55,000 + $30,000 + $10,000 = $95,000

- Beginning Cash Balance = $20,000

- Ending Cash Balance = $20,000 + $95,000 = $115,000

Why It Matters:

A positive net cash flow means a company has more cash coming in than going out, while a negative cash flow may indicate financial strain or growth investments.

Why Understanding These Components Matters?

Helps businesses track cash liquidity and financial stability. Supports investment and expansion decisions. Ensures companies can meet financial obligations without borrowing.

By analyzing the key components of a Cash Flow Statement in Finance and Accounting, businesses can optimize cash management strategies and improve financial performance. The next section will explore different types of cash flow statements and their applications.